Thoughts of The Day: Disney rolls out 'Lojack for kids'; TheFacebook on the block,

According to the President of Disney Online (the group responsible for Disney Mobile), the most attractive set of features the service offers revolve around giving parents more control over how their children use the phones/service. This presumably would include letting parents turn certain features like ring-tone, music, video, and game downloading on/off, as well as perhaps setting text messaging and voice minute limits on each phone.

While all of these features are impressive when taken together, the one single selling point which I think stands out above all the rest is the ability for parents to utilize the phones' on-board GPS systems to locate their children, ala Lojack for vehicles. In a modern world where children, tweens, etc. are all-the-more often left to their own devices/given more independence from their working parents, this feature gives parents a peace of mind not really otherwise available/attractive.

The only real barrier I can see that would keep families with younger children from opting for Disney Mobile would be their hesitation to switch over from their existing family plans with the major carriers. Remember most of these contracts include early opt-out clauses often charging upwards of $150 for early termination, so there is a timing cycle issue. Also, to what extent will adults be willing to themselves carry a Disney-branded cell phone is questionable. Assuming Disney gets the marketing, price points, and perhaps most important, incentive package right, I can see this service becoming fairly popular in the next 12-24 months.

In Other News...

TheFacebook (www.facebook.com), the social networking site popular amongst college students worldwide is said to be up for sale. Rumor has it that the company, started by Harvard undergrads and backed by Accel Partners has already turned down an offer for $750 million. For those who've read my post on MySpace, that company with more registered users, page views, etc fetched a relatively paltry $580 million from Rupert Murdoch's News Corp. back in 2005. Now there are rumors afloat that the company is asking for as much as $2 billion...yes that's Billion, with a "B".

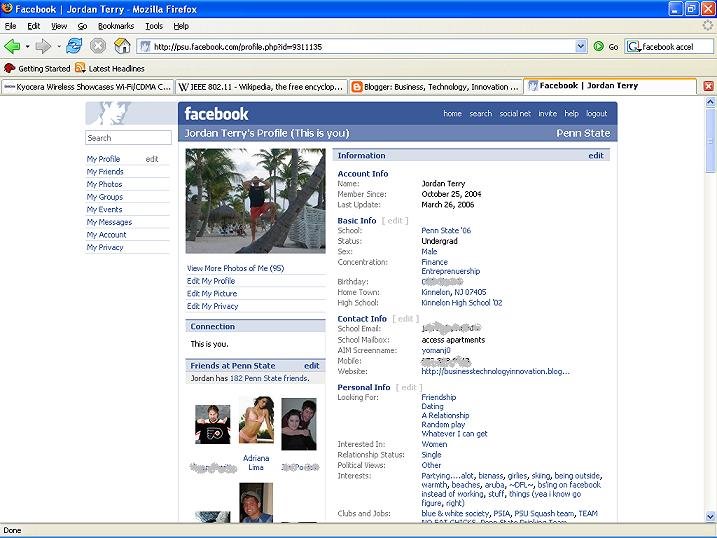

However, while it lacks the broad-based appeal of MySpace (as I pointed out in my criticism of the site a few posts ago), Facebook's interface, layout, and pretty much everything else about it is far cleaner, easier to use, and, not to over-generalize, far less annoying than MySpace (as seen in the above screenshot). Facebook allows users control of the content of their profiles, but does not allow rich media or customized layouts ala MySpace. This results in a globally consistent user experience.

MySpace also leaves something to be desired with its picture offering, limiting the amount of pictures a user can upload via an unsurprisingly awkward upload/captioning process. Facebook has designed and deployed a very clean, intuitive photo service allowing users to create an unlimited number of albums and likewise upload an unlimited number of photos. Not only is the interface and (as it often comes back to, the user experience) far superior than on MySpace, but Facebook also gives users the ability to "tag" their pictures by identifying other Facebook members which appear therein. This makes it easier to find pictures of oneself as well as one's friends.

Facebook also gives users a far better idea of their social network, letting users browse the profiles of all users at their school, as well as users in their classes, social groups, and the actual levels of separation between themselves and other users (through friends of friends, etc). Facebook also has a seldom-talked about graphical network feature, which displays all the connections between ones friends, etc. Again, this beats out MySpace which only really goes so far as to tell you there are somewhere around 29,470,239,508,230,954 people (give or take) in your 'social network', which as far as I can tell is just every registered MySpace user. I could go on and on here, but in general it comes down to design and planning. TheFacebook was clearly well-designed and planned-out every step of the way, whereas MySpace appears to have come to be without any formal system design initiatives being put into place at any step along the way.

Facebook also trounces MySpace when it comes to server/service reliability and latency. Seldom do users suffer from endless wait-times on Facebook and even far more seldom, if ever, does Facebook return 404 or other undeliverable errors. Also, while I don't have the hard statistics, I am certain that the average page file size (kb) on MySpace is far, far smaller than those on MySpace. This is one of the downfalls of MySpace giving end-users complete control over what media they place in their profiles.

Now (drum roll please...), the ultimate reason I think Facebook will fetch the prettier penny:

Data Mining!

That's right folks, TheFacebook is valuable just as much, if not more so for the data locked within its servers as it is for generating ad-based revenues. Because Facebook profiles are essentially records comprised of simple one-word/number or short phrase text strings (the content of which is highly similar across profiles/schools/the entire network), Facebook can easily track incidents of matching strings, as well as trend those incidents. As a matter of fact, every Facebook user has access to Pulse. As seen in the picture below, Pulse shows the most often found strings in each category at one's school (or at any school in the network) versus the entire network as a whole.

Facebook provides this for free to its members! Imagine though if they developed (or have developed) an application allowing marketers - and not just advertisers on the site - to mine this profile data to discover any trends, etc. We're not talking just trends common to all college students in general (although it would certainly be possible), but the ability to drill down to virtually demographic or combined demographic, to say, find differences in popularity of a movie or TV show by region, country, gender, age, or any other field (or combination thereof) in Facebook profiles.

One (or two) more thing(s). Every August, approximately 1,000,000 students begin their collegiate experience. If current penetration levels are any indication then Facebook will capture 800,000 of these students each and every year. Also, many, if not most Facebook users are extremely active. We're talking not only logging in regularly, but multiple times every day. Compare this to, as I again pointed out in a previous post, MySpace, where I'd venture to guess from my experience on that site that the majority of activity is generated by 50% or less of its registered users. So, add users or host billions of impressions or page views across a general and broad population, I see TheFacebook as being potentially far more attractive to not only advertisers, but marketers in general.

So there you have it. About 37 reasons why I would not be surprised to see TheFacebook fetch, oh, lets say somewhere between $900 million - $1.3 Billion. More on this story as it develops. Now stop messing around and get back to work!

posted by Gordon Gekko at

2:45 PM

1 Comments

![]()